Alibaba (NYSE:BABA), the Chinese commerce giant, was founded just 20 years ago but already has over $56 billion in annual revenue, meaning this company moves fast.

And it has a lot of pieces to its puzzle. Tmall, Lazada, Alibaba Cloud, Taobao, and Youku are all subsidiaries worthy of individual investor attention -- not to mention its namesake business Alibaba.com. It's a lot to unpack and can get complicated, especially when you consider the many unique international markets it does business in.

But it's possible to break this down clearly to see whether Alibaba is a buy.

Image source: Getty Images.

The case for Alibaba

Alibaba operates four distinct business segments: commerce, cloud, media/entertainment, and innovation. And the company works in many countries including China, India, Singapore, and Indonesia.

Of these business segments and markets, the most important is Chinese commerce, accounting for 66% of all revenue in fiscal 2019. Chinese commerce has several tailwinds, including overall Chinese economic growth and the country's ever-growing middle class. These make it likely that Alibaba's core business continues to do well.

But it's more than Chinese commerce. In Alibaba's second quarter 2020 earnings call, CEO Daniel Yong Zhang reiterated the company's mission is to "make it easy to do business anywhere." That's a big goal, but it's delivering. For example, the company is leading the way to business digitization through Alibaba Cloud, which grew revenue 64% to $1.3 billion in Q2 and now serves 59% of public Chinese companies.

Another example of making business easy is Lazada's shipping and logistics service for businesses in Southeast Asia. Orders grew over 100% in Q2 year over year.

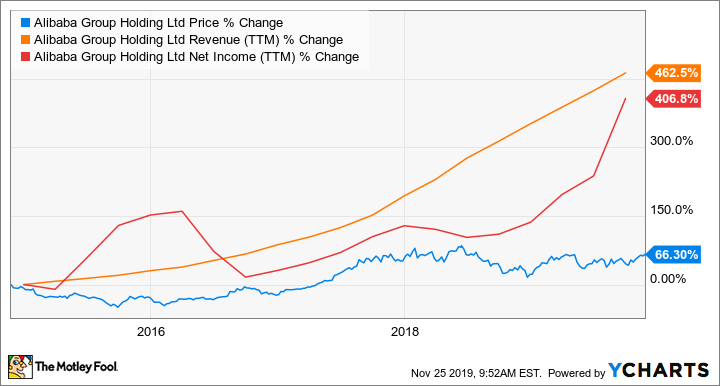

Alibaba has many parts that are growing, which has led to fantastic growth in revenue and net income over the past five years.

BABA data by YCharts. TTM = trailing 12 months.

A stagnant stock price despite robust revenue and net income growth would indicate a cheapening valuation. And that's exactly the case with Alibaba. Despite its outstanding financials and big vision, the stock trades for about 21 times forward earnings. Growth stocks like Alibaba often trade for a much more expensive valuation, suggesting that now may be the time to buy.

The case against Alibaba

Alibaba's stock, as the above chart shows, has traded sideways since January 2018 despite exemplary growth. That's when the tariff war started. Investors are concerned that ongoing tariff pressure could hurt Chinese economic growth. This concern has less to do with Alibaba and more to do with any Chinese stock. However, even though it's not specific to Alibaba, it is relevant.

One of the more Alibaba-specific concerns is its enormous market capitalization of around $500 billion. There are only two companies in the world with a $1 trillion market cap, suggesting that the chances Alibaba can double from here, let alone become a multibagger, are slim.

By way of example, it competes with iQiyi (NASDAQ:IQ) in the video streaming space. iQiyi is the top dog in China with over 100 million subscribers; in its third quarter of 2019, it reported over $1 billion in revenue. That's impressive, but even if Alibaba matched these results, it would only move its quarterly revenue up by around 2%. Simply put, at Alibaba's size, it will be hard to develop new billion-dollar revenue streams at a pace that sustains its current growth rate.

To buy or not to buy?

In reality, the cases for and against Alibaba both have merit. But there are also valid rebuttals to both arguments. If Alibaba's growth is about to slow due to its size and geopolitical pressure, it's not really valid to say that it's "cheap" at a forward P/E of 21. Conversely, it's not reasonable to assume that China and the U.S. will continue to hit each other with tariffs forever.

Rather, I like to zoom out: The big picture is that Alibaba wants to become a global company, and right now the majority of its revenue comes from China. There are plenty of business opportunities outside China. But in China, there's growth opportunity as well. The company currently has 693 million active annual Chinese customers. It's targeting 1 billion customers by 2024 for 44% customer growth in the next five years in China alone.

Finally, the company is well capitalized to continue its winning run. Right now, Alibaba has $33 billion on its balance sheet, and is expected to raise around $13 billion when it has its IPO in Hong Kong. A history of winning and well-funded future opportunities make me call Alibaba a buy today.

"buy" - Google News

November 30, 2019 at 10:48PM

https://ift.tt/2Y0PSL2

Is Alibaba Stock a Buy? - Motley Fool

"buy" - Google News

https://ift.tt/2NAJYvh

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

0 Comments:

Post a Comment