At the start of 2019 Senior Housing Properties Trust(NASDAQ:SNH) was paying a dividend of $0.39 per share per quarter. But just one quarter later it dropped its quarterly disbursement to $0.15 per share, a massive 60% dividend cut. That was a tough call, since management is well aware that dividend investors don't appreciate dividend cuts.

Even with the cut, though, the yield here is still elevated at around 8% (roughly four times the yield of an S&P 500 Index fund). If Senior Housing has regrouped and positioned itself for better days, as management contends, investors might be missing an opportunity here. But what's really going on?

The big, bad cut

Senior Housing Properties Trust is a healthcare real estate investment trust (REIT). It owns a diversified portfolio of assets, including senior housing (around 50% of rent), medical research facilities (27%), and medical office buildings (23%). This isn't materially different from many of the industry's largest players, including Ventas and HealthpeakProperties. So from a portfolio-diversification perspective, Senior Housing Properties is right in-line with peers. In fact, one of the biggest positives here is that medical office and research properties make up roughly half the portfolio. These assets are in high demand right now, and management expects that to remain the case for years to come.

Image source: Getty Images

The other half of the portfolio, however, isn't doing quite as well. The good news is that most of Senior Housing's rent is largely direct pay, so it avoids the issue of Medicare and Medicaid reimbursement changes (which are known as third-party payers). But it hasn't been able to sidestep the overbuilding that has taken place in the senior housing space. And the pain has been widespread.

There are two buckets on the senior housing side of the business: net-lease assets, and what is known as a senior housing operating portfolio (or "SHOP"). Net-lease assets are rented out by other companies under long-term leases. SHOP assets are owned and operated by Senior Housing Properties, though it really hires other companies to do the day-to-day work. The key difference is that the REIT benefits from the operating upside in the SHOP portfolio during good years, while also feeling the pain of the downside in bad years. It just collects rent from a net-lease tenant, though, meaning the tenant takes on all of the operating risks.

The problem today is that there's been a lot of bad news in senior housing, most of which ties back to overbuilding. The long-term story is that the giant baby boomer generation is cresting into retirement, and that will eventually lead to increasing demand for senior housing assets like Senior Housing Properties owns. That's just demographics. But everyone is well aware of the trend, and that predictably led to a material increase in construction in the senior housing space.

That construction is currently starting to come online, increasing competitive pressures in the industry. It has been particularly bad for Senior Housing Properties, whose SHOP portfolio saw net operating income (NOI) fall 17.5% year-over-year in the third quarter. That's much worse than at its larger peers, where declines were closer to 5%. Still, in a difficult market, investors would expect the SHOP portfolio to take a hit. The real concern is that Senior Housing Properties' net lease portfolio saw NOI drop even further, declining 30% year-over-year.

There's a story behind that number, and it helps explain both the dividend cut at the start of the year and the concerns that investors still appear to have about Senior Housing Properties' future.

Helping out a troubled tenant

A large portion of Senior Housing's net-lease assets are run by a company called Five Star Senior Living. It was having a particularly hard time dealing with the supply/demand imbalance from overbuilding, and Senior Housing Properties effectively ended up recapitalizing the company. In a complex deal, Senior Housing provided rent concessions and a cash infusion. That helps explain the massive year-over-year NOI decline in the net-lease portfolio in the third quarter, and why Senior Housing had to cut its dividend.

The deal, however, gets even more complicated. Five Star is giving equity to Senior Housing Properties, increasing its ownership of Five Star, and also issuing shares to Senior Housing Properties' shareholders. As if that weren't enough, the assets Five Star leased will no longer be net-lease assets, and will instead shift into the SHOP portfolio when all is said and done. There are a lot of moving parts in this complicated agreement, but the end result is that Senior Housing's SHOP portfolio will expand from 77 properties out of 286 senior housing assets (27%) to 243 out of 286 (85%).

The deal won't be fully complete until early 2020, but this is a material change. And even at that point there will be more work ahead, because Senior Housing plans to sell off nearly $1 billion worth of poorly performing assets. But the big story is that this move, while perhaps necessary to avoid the bankruptcy of a key lessor, materially increases the risk for Senior Housing Properties. It will now be participating a lot more in the performance of its senior housing assets. Right now that seems like a bad thing, since the industry is facing a supply/demand imbalance caused by overbuilding. As long as that imbalance continues, near-term results here aren't likely to be very good.

That said, with the dividend cut Senior Housing Properties now has one of the lowest payout ratios in the industry, and its dividend is arguably in a strong position to weather the current market headwinds. And while supply and demand are out of whack right now, the long-term demographics haven't materially changed, so increased demand is still coming. Meanwhile, the current industry headwinds have led to a drop in construction, which should further help to alleviate the supply/demand imbalance over time. So there's a reason to buy into the idea that Senior Housing Properties has made the hard call, and once it's through this rough patch the future looks much brighter.

However, until the dust settles on this complex deal, most investors are still probably better off sitting on the sidelines. There's just too much going on. That includes the not-so-subtle fact that the same company that struggled to operate properties profitably as a net-lease tenant is now going to be operating those same properties under contract for Senior Housing's SHOP portfolio. Maybe Five Star can turn things around, but until there's proof that this plan is more than a band-aid, it is way too early to call it a successful resolution.

Too many questions, not enough answers

Senior Housing Properties has made a bold move to deal with a very big issue. That decision has resulted in investors having to swallow a huge dividend cut, and what appears to be a material increase in risk, as the SHOP portfolio expands. Until its efforts to help right Five Star play out for a little while, most investors should probably avoid Senior Housing Properties. Yes, the 8% yield is enticing, but it comes with a lot of risk. The trade-off just doesn't seem worthwhile at this juncture.

Like its giant rivals, British American Tobacco(NYSE:BTI) dodged several bullets recently when President Trump decided to back away from a complete ban on flavored e-cigarette liquids, and the Food and Drug Administration temporarily shelved plans for tough new regulations on nicotine in traditional cigarettes.

Both actions should help the cigarette leader continue generating profitable sales, even though one of those businesses is under greater scrutiny by regulators and the other is suffering the effects of the secular decline of the industry.

So let's look at whether investors should consider British American Tobacco stock a buy.

Image source: Getty Images.

Smoke 'em if you got 'em

The tobacco industry is a lot more diversified and nuanced than it was when simply producing cigarettes was the norm. While the number of players is much more concentrated due to mergers and acquisitions, the kinds of products and technological advances they offer are much broader. And British American Tobacco has a leading role in most of them, if not all.

The cigarette leader divides its business into two segments: traditional cigarettes (what it calls strategic combustibles), and potentially reduced-risk products like e-cigarettes, snus, and the fastest growing segment of the tobacco products market, nicotine pouches.

Combustibles are what pay the bills, accounting for 64% of British American's total revenue, or almost $7.8 billion. Yet they're also in a significant decades-long decline.

The Centers for Disease Control and Prevention says the number of adults who smoke has tumbled from 42.4% of the U.S. population in 1965 to just 14% in 2017, and British American's cigarette volumes are down 3.7% year to date.

According to the most recent data from Nielsen, traditional cigarette sales tumbled 6.8% during October, which follows a 7.3% drop in August. The declines comes as cigarette companies have hiked prices three times this year, an unusual occurrence that was started by Altria(NYSE:MO) as it tried to make up for falling volume last year.

An e-cig warning sign

Although the drops seem steep, they ameliorated somewhat as federal regulators responded to an outbreak of lung illnesses caused by vaping that led to thousands being injured and dozens of people dying. Despite having an inkling early on that the cause was illicit vaping e-liquids sold on the internet, something they've all but nailed down as the culprit, regulators continue to advocate that people give up vaping altogether.

It seems to have had an impact on sales. Year-over-year e-cig volumes went from being up over 60% in August to rising just 18% by October.

Hardest hit was Juul Labs, the leading e-cig maker, which saw its volume growth slow from a 50% increase in August to a 3.9% decline in October. Not only did it stop selling flavored pods for its e-cig during that time, which hurt sales, but the Juul device was also the one singled out most often by those who had fallen ill.

That creates a big opportunity for British American Tobacco, as it recently submitted to the FDA its pre-market tobacco application (PMTA) for its Vuse e-cig. Only Philip Morris International(NYSE:PM) submitted and had approved a PMTA, for its IQOS device, and other makers may not be able to afford or handle the complexity of the process. If British American can make it through the regulatory labyrinth, it may be one of only a select few allowed on the market.

Currently Vuse is the third largest e-cig with around a 10% share, down sharply from the 17% share it held two years ago when it was the second biggest. It's been eclipsed by NJOY, which has taken to steeply discounting its e-cigs, selling them for $0.99 in stores. In comparison, a Juul sells for around $35.

The tactic is working as NJOY went from less than 2% market share to second place with an 11.6% share. British American has now also begun cutting the price of its e-cigs, selling its Vuse Alto brand for $0.99, down from $25. While that may help it maintain or even boost its market share, it's going to cut into profits. Unlike combustibles, where tobacco companies can almost raise prices at will, e-cigs don't have that same kind of pricing power.

A price worth paying

Many investors, however, come to British American Tobacco for its dividend, which currently yields a robust 6.9% annually. Yet its payout ratio is 65%, which is on the high side. It's not wholly unsustainable for this company, but with declining cigarette volumes and the need to sell its e-cigs at a huge discount, it may not be a smooth ride, either.

What it has going for it are leading cigarette brands and the potential to be one of just a handful of e-cig companies with products on the market. It's not the same landscape as when British American Tobacco was simply selling cigarettes and chewing tobacco, but it's one where its stock can still be considered a buy.

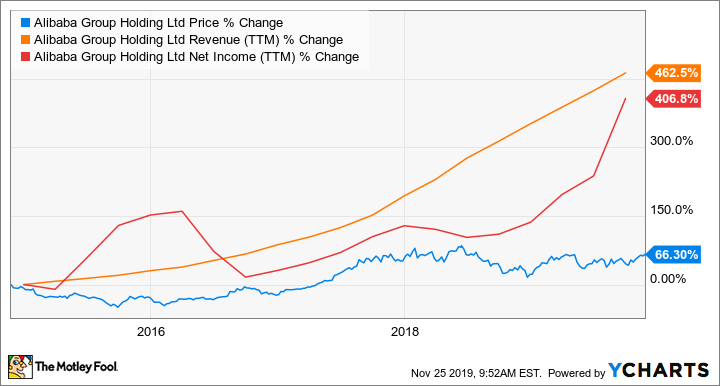

Alibaba(NYSE:BABA), the Chinese commerce giant, was founded just 20 years ago but already has over $56 billion in annual revenue, meaning this company moves fast.

And it has a lot of pieces to its puzzle. Tmall, Lazada, Alibaba Cloud, Taobao, and Youku are all subsidiaries worthy of individual investor attention -- not to mention its namesake business Alibaba.com. It's a lot to unpack and can get complicated, especially when you consider the many unique international markets it does business in.

But it's possible to break this down clearly to see whether Alibaba is a buy.

Image source: Getty Images.

The case for Alibaba

Alibaba operates four distinct business segments: commerce, cloud, media/entertainment, and innovation. And the company works in many countries including China, India, Singapore, and Indonesia.

Of these business segments and markets, the most important is Chinese commerce, accounting for 66% of all revenue in fiscal 2019. Chinese commerce has several tailwinds, including overall Chinese economic growth and the country's ever-growing middle class. These make it likely that Alibaba's core business continues to do well.

But it's more than Chinese commerce. In Alibaba's second quarter 2020 earnings call, CEO Daniel Yong Zhang reiterated the company's mission is to "make it easy to do business anywhere." That's a big goal, but it's delivering. For example, the company is leading the way to business digitization through Alibaba Cloud, which grew revenue 64% to $1.3 billion in Q2 and now serves 59% of public Chinese companies.

Another example of making business easy is Lazada's shipping and logistics service for businesses in Southeast Asia. Orders grew over 100% in Q2 year over year.

Alibaba has many parts that are growing, which has led to fantastic growth in revenue and net income over the past five years.

A stagnant stock price despite robust revenue and net income growth would indicate a cheapening valuation. And that's exactly the case with Alibaba. Despite its outstanding financials and big vision, the stock trades for about 21 times forward earnings. Growth stocks like Alibaba often trade for a much more expensive valuation, suggesting that now may be the time to buy.

The case against Alibaba

Alibaba's stock, as the above chart shows, has traded sideways since January 2018 despite exemplary growth. That's when the tariff war started. Investors are concerned that ongoing tariff pressure could hurt Chinese economic growth. This concern has less to do with Alibaba and more to do with any Chinese stock. However, even though it's not specific to Alibaba, it is relevant.

One of the more Alibaba-specific concerns is its enormous market capitalization of around $500 billion. There are only two companies in the world with a $1 trillion market cap, suggesting that the chances Alibaba can double from here, let alone become a multibagger, are slim.

By way of example, it competes with iQiyi(NASDAQ:IQ) in the video streaming space. iQiyi is the top dog in China with over 100 million subscribers; in its third quarter of 2019, it reported over $1 billion in revenue. That's impressive, but even if Alibaba matched these results, it would only move its quarterly revenue up by around 2%. Simply put, at Alibaba's size, it will be hard to develop new billion-dollar revenue streams at a pace that sustains its current growth rate.

To buy or not to buy?

In reality, the cases for and against Alibaba both have merit. But there are also valid rebuttals to both arguments. If Alibaba's growth is about to slow due to its size and geopolitical pressure, it's not really valid to say that it's "cheap" at a forward P/E of 21. Conversely, it's not reasonable to assume that China and the U.S. will continue to hit each other with tariffs forever.

Rather, I like to zoom out: The big picture is that Alibaba wants to become a global company, and right now the majority of its revenue comes from China. There are plenty of business opportunities outside China. But in China, there's growth opportunity as well. The company currently has 693 million active annual Chinese customers. It's targeting 1 billion customers by 2024 for 44% customer growth in the next five years in China alone.

Finally, the company is well capitalized to continue its winning run. Right now, Alibaba has $33 billion on its balance sheet, and is expected to raise around $13 billion when it has its IPO in Hong Kong. A history of winning and well-funded future opportunities make me call Alibaba a buy today.

Since Google bought Fitbit, people seem to have fallen into one of two categories: Those who don’t care at all about the privacy implications, and those very much do. For the latter, it means this holiday season is a good chance to jump on sales and buy a replacement smartwatch or tracker. But which one?

While Gizmodo does have a pretty great buying guide (curated by yours truly), it features Fitbits in many of the categories. Because let’s face it, privacy concerns aside, Fitbit knows what it’s doing when it comes to hardware. Its software is also super streamlined and easy to use for general tracking. Only, while Fitbits is the shorthand term people use to describe this category of gadgets, they’re not the be-all, end-all.

Advertisement

A quick aside here: Privacy when it comes to your health data is a lot of smoke and mirrors. All these companies have published their own privacy policies, but many are also complicit in corporate wellness programs with employers and insurers. Using a tracker or smartwatch to monitor your health will require you to at least acknowledge that your information—albeit aggregated and anonymized—will be used for profit. It’s a definite tradeoff, but only you can decide whether, say, the convenience of tracking your period via your wrist is worth giving that sensitive data to any company at all. I’ve written about why it’s sort of hypocritical to be up in arms about Google owning Fitbit data when Fitbit’s already been profiting off it for years. That said, I get the legitimate concern. Plus there’s plenty of us out there who are irrevocably hooked in this self-quantifying game and want alternatives.

Many readers have commented this is why it’s a good time to jump ship for the Apple Watch. Apple has done a good job marketing itself as the One Company That Cares About Your Privacy. That’s sort of true. Apple is better than most, but again, it participates in corporate wellness programs too. And, if you participate in its research studies, you are consenting to give your data to third-parties of some sort. However, if you’re an iOS user looking for a smartwatch experience, the Series 5 is hard to beat. Its always-on display is better than the Fitbit Versa 2's, and recent software updates to the Health and Activity app have improved data contextualization on the platform as a whole.

But recommending the Apple Watch is also trite and leaves out the thousands of Android users. Plus, the Apple Watch starts at $400, which is expensive as hell unless you’re willing to opt for a discounted Series 3. To be clear, the Series 3 is still a great watch but doesn’t come with the latest display or ECG features. If you’re looking to replace a Versa, the Samsung Galaxy Watch Active2 is a decent choice. It is packed with fitness features, and Tizen OS is leagues better than Google’s WearOS. (Also, pretty sure the whole point of replacing Fitbits is to get away from Google, so...) I had accuracy issues when I tested it, but Samsung has updated its software since then.

Advertisement

But the most 1:1 competitor with Fitbit is probably Garmin. On the data front, you’ll get way more in-depth metrics and this past summer, Garmin finally updated its smartwatch line so it doesn’t look quite as hideous anymore. The Venu, its first AMOLED smartwatch, is pretty snazzy. Meanwhile, its hybrid analog Vivomove line is just plain gorgeous. There’s also the Vivosmart and Vivofit lines, which serve as basic trackers. One important note—particularly if you’re on a budget—almost all these options are more expensive than the corresponding Fitbits.

That brings me to the sea of cheap fitness trackers that have chipped away at Fitbit’s dominance over the last few years. While I think the Fossil Hybrid HR is a worthy successor to Pebble, many Pebble fans have since let me know that the Amazfit Cor or Amazfit Bip also fills the niche for simple, attractive trackers that don’t cost an arm and a leg. And I’d be remiss if I didn’t mention the Xiaomi Mi Band 4, which is stupid cheap at $40 and tracks basically everything the Fitbit Inspire HR does.

Advertisement

All these products have their individual quirks. Most don’t have the community aspect Fitbit does. So while challenges are built into some of them, like the Garmins, the devices just aren’t as ubiquitous. Fitbit’s app also doesn’t give you the most detailed stats—not to mention they’ve now started locking behind more meaningful data behind a subscription—but it is a well-designed app. Some of the others (especially budget options) are, well, still working on that. However, most of the smartwatches I mentioned are just as good, if not better, than the Versa. As for the basic trackers, they’ll give you a comparable experience with regard to accuracy—and that’s sort of the point, isn’t it?

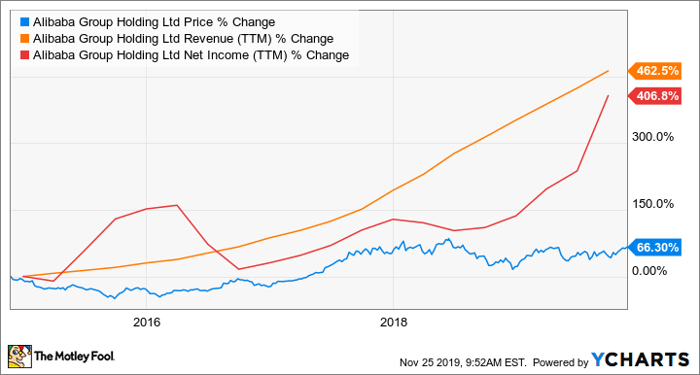

Alibaba(NYSE: BABA), the Chinese commerce giant, was founded just 20 years ago but already has over $56 billion in annual revenue, meaning this company moves fast.

And it has a lot of pieces to its puzzle. Tmall, Lazada, Alibaba Cloud, Taobao, and Youku are all subsidiaries worthy of individual investor attention -- not to mention its namesake business Alibaba.com. It's a lot to unpack and can get complicated, especially when you consider the many unique international markets it does business in.

But it's possible to break this down clearly to see whether Alibaba is a buy.

Image source: Getty Images.

The case for Alibaba

Alibaba operates four distinct business segments: commerce, cloud, media/entertainment, and innovation. And the company works in many countries including China, India, Singapore, and Indonesia.

Of these business segments and markets, the most important is Chinese commerce, accounting for 66% of all revenue in fiscal 2019. Chinese commerce has several tailwinds, including overall Chinese economic growth and the country's ever-growing middle class. These make it likely that Alibaba's core business continues to do well.

But it's more than Chinese commerce. In Alibaba's second quarter 2020 earnings call, CEO Daniel Yong Zhang reiterated the company's mission is to "make it easy to do business anywhere." That's a big goal, but it's delivering. For example, the company is leading the way to business digitization through Alibaba Cloud, which grew revenue 64% to $1.3 billion in Q2 and now serves 59% of public Chinese companies.

Another example of making business easy is Lazada's shipping and logistics service for businesses in Southeast Asia. Orders grew over 100% in Q2 year over year.

Alibaba has many parts that are growing, which has led to fantastic growth in revenue and net income over the past five years.

A stagnant stock price despite robust revenue and net income growth would indicate a cheapening valuation. And that's exactly the case with Alibaba. Despite its outstanding financials and big vision, the stock trades for about 21 times forward earnings. Growth stocks like Alibaba often trade for a much more expensive valuation, suggesting that now may be the time to buy.

The case against Alibaba

Alibaba's stock, as the above chart shows, has traded sideways since January 2018 despite exemplary growth. That's when the tariff war started. Investors are concerned that ongoing tariff pressure could hurt Chinese economic growth. This concern has less to do with Alibaba and more to do with any Chinese stock. However, even though it's not specific to Alibaba, it is relevant.

One of the more Alibaba-specific concerns is its enormous market capitalization of around $500 billion. There are only two companies in the world with a $1 trillion market cap, suggesting that the chances Alibaba can double from here, let alone become a multibagger, are slim.

By way of example, it competes with iQiyi(NASDAQ: IQ) in the video streaming space. iQiyi is the top dog in China with over 100 million subscribers; in its third quarter of 2019, it reported over $1 billion in revenue. That's impressive, but even if Alibaba matched these results, it would only move its quarterly revenue up by around 2%. Simply put, at Alibaba's size, it will be hard to develop new billion-dollar revenue streams at a pace that sustains its current growth rate.

To buy or not to buy?

In reality, the cases for and against Alibaba both have merit. But there are also valid rebuttals to both arguments. If Alibaba's growth is about to slow due to its size and geopolitical pressure, it's not really valid to say that it's "cheap" at a forward P/E of 21. Conversely, it's not reasonable to assume that China and the U.S. will continue to hit each other with tariffs forever.

Rather, I like to zoom out: The big picture is that Alibaba wants to become a global company, and right now the majority of its revenue comes from China. There are plenty of business opportunities outside China. But in China, there's growth opportunity as well. The company currently has 693 million active annual Chinese customers. It's targeting 1 billion customers by 2024 for 44% customer growth in the next five years in China alone.

Finally, the company is well capitalized to continue its winning run. Right now, Alibaba has $33 billion on its balance sheet, and is expected to raise around $13 billion when it has its IPO in Hong Kong. A history of winning and well-funded future opportunities make me call Alibaba a buy today.

10 stocks we like better than Alibaba Group Holding Ltd.

When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has quadrupled the market.*

David and Tom just revealed what they believe are the ten best stocks for investors to buy right now... and Alibaba Group Holding Ltd. wasn't one of them! That's right -- they think these 10 stocks are even better buys.

אחרי דיכוי המהומות: צרפת וגרמניה מאותתות על שינוי היחס כלפי איראן - ישראל היום

לראשונה מאז החליט ממשל טראמפ לסגת מהסכם הגרעין עם איראן, מבהירות שתי שותפות אירופיות בכירות להסכם כי סבלנותן פוקעת לנוכח ההפרות הנמשכות של ההסכם מצד טהרן, וכי הן שוקלות להמליץ על חידוש הסנקציות הבינלאומיות על איראן.

"נפעל ליצירת סנקציות חסרות תקדים נגד איראן"

לפי סעיף זה, יובא כל סכסוך הנוגע להפרת ההסכם בפני ועדה של נציגי המעצמות והאיחוד האירופי, החתומים על ההסכם. אם לא תושג הסכמה בין הצדדים שאיראן מפרה את ההסכם יועבר הנושא לדיון בפני מועצת הביטחון של האו״ם. אם זו לא תקבל החלטה תוך 30 יום על עיצומים חדשים, ייכנסו מחדש לתוקף כל העיצומים הבינלאומיים שהוטלו על איראן על ידי מועצת הביטחון לפני חתימת הסכם הגרעין.

לה-דריאן הדגיש, שלמרות הניסיונות של האירופים לקדם יוזמות שיאפשרו לשמר את הסכם הגרעין למרות עזיבת ארה״ב, איראן נקטה שורת צעדים שהכשילו את המהלכים הללו, ובכלל זה הדיכוי הקטלני של הפגנות המחאה ברחבי איראן על עליית מחירי הדלק, והתקפת מתקני הנפט בסעודיה.

לדברי שר החוץ הצרפתי, היקף דיכוי ההפגנות מנע ניסיונות אירופיים לשכנע את ארה״ב לפעול למניעת הסלמה נוספת מול איראן. ״ההתנהגות של המנהיג העליון ח׳מינאי והנשיא רוחני כלפי המפגינים, הוכיחה לאמריקנים את צדקת גישתם של ׳לחץ מירבי׳ על איראן״, הדגיש לה-דריאן.

גם בכירים בממשלת גרמניה מדברים על הפעלתו של מנגנון חידוש הסנקציות הנכלל בהסכם הגרעין לנוכח ההפרות המתרבות מצדה של איראן. ״אם סוכנות האנרגיה הגרעינית של באו״ם תשוב ותדווח על הפרות איראניות של הסכם הגרעין, נהיה חייבים להגיב״, אומר ל״ישראל היום״ גורם ממשלתי בכיר.

כוחות הביטחון באיראן מול המפגינים // צילום: AP

״הפעלת לחץ על איראן תמיד הייתה המדיניות של גרמניה. גם הסכם הגרעין לא היה הסכם ידידות אלא נבע מרצון לנסות למנוע התגרענות צבאית איראנית, שהייתה מהווה איום גם על אירופה. ניסינו עם הצרפתים להביא את האיראנים להסכים על פשרות מול האמריקנים, והמאמצים הללו נכשלו. אנחנו צריכים לחשוב היטב, מה יהיו הצעדים הבאים שלנו. המחאה העממית היא אתגר רציני, אך היא אינה מערערת את המשטר. ׳מערכות הצללים׳ - משמרות המהפכה ושליחי איראן ברחבי המזה״ת מתחזקים במצבים דרמטיים מסוג זה, ולא ניתן להעריך איך הם יגיבו. המצב במזה״ת מאוד מסוכן ויכול לצאת מידי שליטה. הקשרים שלנו עם טהרן מאפשרים לנו לשמור על ערוצים פתוחים עם איראן״.

עם זאת, ביום ששי הודיעו שש מדינות אירופיות נוספות - הולנד, בלגיה, פינלנד, דנמרק, שוודיה ונורבגיה - על הצטרפותן למנגנון עקיפת העיצומים הפיננסיים שהטילה ארה״ב על איראן (״אינסטקס״). מנגנון זו הוקם ביוזמת האיחוד האירופי על ידי צרפת, גרמניה ובריטניה, במטרה לסייע לכלכלה האיראנית להתמודד עם העיצומים האמריקניים ולאפשר לחברות אירופיות להמשיך לעשות עסקים עם איראן. שש המדינות הבהירו שהמהלך נועד לחזק את התמיכה האירופית בהסכם הגרעין ולאפשר לאיראן ליהנות מפירותיו הכלכליים של הסכם הגרעין.

יצוין עוד, כי למרות רצח כ-150 מפגינים בידי המשטר האיראני במהלך גל המחאה העממי האחרון, התארח בברלין בשבוע שעבר סגן שר החוץ האיראני, סייד מוחמד קאסם סיאדפור, המכהן גם כנשיא מכון המחקר לעניינים פוליטיים ואסטרטגיים המסונף למשרד החוץ בטהרן. סיאדפור הגיע לבירת גרמניה על מנת להשתתף בפורום בינלאומי על מדיניות חוץ, פורום הממומן בחלקו על ידי ממשלת גרמניה.

Shopify(NYSE:SHOP) and Veeva Systems(NYSE:VEEV) have crushed the market recently, and both have plenty of potential to continue to do so going forward. Nonetheless, one of these stocks will be a superior investment to the other. Let's see if we can figure out which one.

We'll judge these stocks on the basis of seven criteria, giving each category equal weight.

Image source: Getty Images.

1. Stock appreciation

Over the last five years, Shopify has returned 1,011% to its investors since its initial public offering. Veeva Systems has returned 445% over that same five-year period. The S&P 500, by contrast, only returned 46% in that time span. Both stocks really spanked the market; Veeva Systems did 10 times better than the market, and Shopify did 22 times better.

Winner: Shopify

2. Rule of 40

Venture capitalists have a quick and dirty method for valuing software-as-a-service (SaaS) companies, particularly when they are fast-growing and unprofitable start-ups. It's a simple calculation: Add a company's profit margin and revenue growth together. If the sum of those two numbers is higher than 40, you have a winner.

Shopify's revenue growth has recently slowed to 44%. While that's still amazing growth, it's only half of our calculation. Unfortunately, Shopify remains unprofitable, with a profit margin of negative 9%. After adding the two numbers together, our "rule of 40" calculation gives us 35, which is not a passing grade.

At 27%, Veeva System's revenue growth is not bad, and its profit margin is terrific, at 30%. Adding those two numbers together gives Veeva a "rule of 40" score of 57. Ding ding!

Winner: Veeva Systems

3. Market cap and total addressable market

Our third criterion is an estimation of how big a company can get. Another way of thinking about this is how high the stock can go. Market capitalization often provides a ceiling for growth, and your stock might start bumping into it. It's harder for a company with a trillion-dollar market cap to double again and again than it is for a much smaller company.

A company's total addressable market (TAM) can also be a limitation. If a company is going after a small market opportunity, then the upside to the stock is limited. However, if a company is going after a huge market, then your stock growth is open-ended. Keeping TAM in mind can help you avoid niche businesses and instead focus on companies with realistic chances of making 10, 40, or maybe even 100 times your money.

Shopify and Veeva Systems are both large-cap companies, with market caps of $37 billion and $23 billion, respectively. Veeva provides a SaaS solution for the life sciences industry. The company provides very specific software solutions for pharmaceutical companies and medical device companies. Its software provides solutions that healthcare companies find invaluable in areas like research, clinical trials, and drug sales.

Going after a vertical like this gives Veeva powerful advantages within that vertical, but it also limits the market opportunity. Right now, Veeva Systems only has 719 customers. That's a small number. Veeva estimates its TAM at $9 billion. While Veeva hopes to expand into other industry verticals, like cosmetics and chemicals, right now, the company is clearly a niche business.

Shopify's TAM, on the other hand, is potentially much larger. Any company who wants to do business on the internet is a possible customer. Shopify estimates its market opportunity for small businesses at $70 billion dollars. Shopify also is seeing subscriptions from entrepreneurs who are just starting out as well as large businesses. The market opportunity is vast. Shopify just recently announced that the company had over a million merchants on its network.

Winner: Shopify

4. Cash and debt

This is an easy one to run down. In the most recent quarter, Shopify had $2.67 billion in cash and $111 million in debt. Subtract the debt from the cash, and Shopify has $2.56 billion in net cash.

In its most recent quarter, Veeva Systems reported $1.43 billion in cash and $22 million in debt. Subtract the debt from the cash, and Veeva has $1.41 billion in net cash.

Both of these companies have outstanding numbers, but Shopify has over $1 billion more in net cash than Veeva, so we'll call it the winner.

Winner: Shopify

5. Leadership

What we like to see here is a founder-led business, somebody with high insider ownership that gives the founder skin in the game. Leadership really answers the question, "Do I want to invest in this business?" Leadership also defines culture, answering what it would be like to work there. Tobi Lutke is the founder and CEO of Shopify. He has significant ownership stakes in Shopify and is now a billionaire because of his vision and execution. Lutke talks about his company's culture in this fantastic interview.

Peter Gassner is a co-founder and CEO of Veeva Systems. Like Lutke, he's a billionaire now because of his shares in the company he created. According to Forbes, Gassner flies coach and rides a bike to work. Both have strong attributes and lead their companies well.

Winner: tie

6. Competitive and regulatory threats

Amazon was an early competitor to Shopify, and the e-commerce giant gave up, surrendered, and left the field of battle. Amazon, of course, is a fantastic company that's conquering the world of internet retail. To have Amazon enter your market, try to compete with you, and then run away is impressive.

Meanwhile, Veeva Systems has vaulted from the No. 9 company in its life sciences niche (in 2012) to the No. 1 company five years later. It replaced general software offerings from Oracle and SAP with a specific suite of software designed to help pharmaceutical companies.

Both Shopify and Veeva have impressive mindshare in their respective markets, and though neither company is a monopoly yet, they're both on their way. So far, the Department of Justice hasn't had to file any complaints or tried to break either company up.

Winner: tie

7. Share price and valuation

Shopify shares currently trade at a sky-high multiple of more than 300 times forward earnings. Also, the company's shares are selling for 29 times its revenue, which is also high.

Veeva Systems sits at a high but still slightly more reasonable 60 times forward earnings, and the company is selling for 23 times its revenue.

Winner: Veeva Systems

And the winner is...

Shopify wins in a squeaker. Both of these companies are outstanding businesses in the SaaS market, which is arguably the strongest of all business models. Companies with high multiples like these often get hit hard during recessions. But make no mistake, these are both powerful businesses and wonderful stocks.

בלונדון שיבחו את עוברי האורח שהשתלטו על המחבל: "גבורה עוצרת נשימה"

פוליטיקאים ואנשי ציבור בריטים שיבחו היום (שבת) את עוברי האורח שפעלו אתמול ב"גבורה עוצרת נשימה" כשהשתלטו על הדוקר בפיגוע בגשר לונדון. יממה לאחר מתקפת הטרור בבירה, הותר לפרסום שמו של אחד משני הנרצחים - ג'ק מריט, עובד באוניברסיטת קמברידג' שהנחה כנס אליו הגיע המחבל, אוסמאן חאן.

חאן, שעטה על גופו חגורת נפץ מזויפת, החל לדקור עוברי אורח על הגשר המפורסם. בסרטונים שפורסמו ברשתות החברתיות נראו כמה בני אדם מתנפלים על הדוקר עד שכוחות המשטרה הגיעו לזירה וירו בו למוות. שלושה פצועים נוספים עדיין מאושפזים בבתי החולים.

עוד בוואלה! NEWS

ראש הממשלה בוריס ג'ונסון הודה לאזרחים שהצליחו להשתלט על המחבל. "אני רוצה להוקיר את האומץ יוצא הדופן של אותם אזרחים שהתערבו ובגופם הצליחו להציל חיי אחרים", אמר. "עבורי הם מייצגים את הטוב במדינה שלנו ואני מודה להם בשם מדינתנו".

ראש עיריית לונדון סאדיק חאן הבהיר כי אותם אזרחים שהתעמתו עם התוקף לא ידעו כי חגורת הנפץ על גופו הייתה תרמית. "מה שמדהים בתמונות שראינו הוא הגבורה עוצרת הנשימה של האזרחים שרצו לכיוון הסכנה מבלי לדעת מי עומד מולם", תיאר ראש העיר. "הם באמת טובי בנינו".

המלכה אליזבת מסרה את תנחומיה למשפחות הקורבנות. בהודעה מטעמה נכתב כי היא שולחת "מחשבותיה, תפילותיה ותנחומיה העמוקים לאלו שאיבדו את יקיריהם" במתקפה בגשר לונדון.

בתיעוד נראה אחד מעוברי האורח כשהוא מתרחק מההמולה לאחר שהצליח לקחת את הסכין מידי הדוקר, שנותר שכוב על הרצפה, ודוחק בהמון לעזוב את המקום. ג'ורג' רוברטס, ששהה על הגשר באותו הזמן, אמר כי האדם האלמוני חצה במהירות התנועה הסואנת והזדרז להתעמת עם המחבל, יחד עם כמה אזרחים נוספים. "נמלטנו אבל נראה כי הוא נטרל אותו. זאת גבורה מדהימה", צייץ רוברטס בטוויטר.

משתמשים נוספים בטוויטר שיבחו את גיבור היום שהצליח לחלץ את הסכין. הגולשים הציעו לוותר לו על תשלום המשכנתה, בעוד אחרים טענו כי הוא לא צריך יותר לשלם עבור משקה לעולם.

רוב אנדרווד, בן 65 שביקר בלונדון, שחזר כי שמע פיצוצים ובתחילה לא היה בטוח כי אלה קולות ירי. "ברגע שראיתי את כולם ממהרים להימלט התחלתי לפחד ואני חושב שהדבר העיקרי היה לברוח", סיפר לסוכנות הידיעות רויטרס. "הרגשתי ממש מפוחד ולחוץ לגבי המתרחש ורק חיכיתי שהעניין יחלוף".

אוניברסיטת ביר זית: כך חמאס מגייס סטודנטים פלסטינים - וואלה!

הטבות תמורת טרור: כך חודר חמאס לתאי הסטודנטים הפלסטינים בגדה

(בווידיאו: המסתערבים שנטמעו באוניברסיטת ביר זית טרם מעצרו של קיסוואני, מרץ 2018)

יו"ר הרשות הפלסטינית אבו מאזן מתקרב ליום הולדתו ה-85, ומצבו הבריאותי מידרדר משנה לשנה, בלשון המעטה. מנגנוני הביטחון הפלסטיניים יודעים היטב כי אם יש גורם מרכזי שינסה לערער על יציבותה של הרשות הפלסטינית - זו תהיה תנועת חמאס, שמפיחה רוח ומקדמת פעילות באמצעות זרמי עומק. אחד מהבולטים בזרמים אלה הם אגודות הסטודנטים הנאמנות לחמאס. לכן, הסטודנטים נמצאים בפיקוח פלסטיני מתמיד שנועד לאתר דמויות מפתח בשורותיהם.

עם זאת, ההיסטוריה הוכיחה שהפיקוח הזה לא תמיד יעיל. כדי שפיגוע לא יחמוק תחת הרדאר, מפעיל צה"ל והשב"כ משאבים רבים וחשיבה כדי לאתר את הדמויות הבולטות ביותר. מדובר באותם סטודנטים שלא רק יקראו תיגר על הנהגת הפתח וינסו להניע השתלטות או הפיכה - אלא גם ינסו לבצע פיגועי טרור בטווח המיידי. אף שמדובר בסטודנטים בודדים, מתי מעט מתוך אלפים רבים, הפוטנציאל שלהם עלול להיות קטלני.

עוד בוואלה! NEWS

יו"ר אגודת הסטודנטים וראש תא חמאס באוניברסיטת ביר זית שצפונית לרמאללה, עומר קיסוואני, היה הרבה זמן על הכוונת של מערכת הביטחון. כשנערם מידע מודיעיני משמעותי על פעילותו בשנת 2018 הוחלט לעצור אותו בצו מנהלי. בפעם הראשונה, הוא חמק ברגע האחרון בשעת לילה מדירתו בשכונת מסיון ברמאללה. בפעם השנייה הוא נמלט מכוח צבאי בכניסה לקמפוס. בפעם השלישית הוחלט במערכת הביטחון לא לקחת סיכונים. מעצרו בוצע ב-7 במרץ 2018 על ידי יחידת המסתערבים של משמר הגבול, לאור יום ובין כותלי האוניברסיטה.

המבצע היה מוקפד ולא השאיר לקיסוואני פתחי מילוט. לפי עדויות שפורסמו בכלי התקשורת הפלסטיניים, ותיעוד הסטודנטים ההמומים, נכנסו לוחמי יחידת המסתערבים לתוך הקמפוס כשהם לבושים בבגדי אזרחים, מתנהלים כסטודנטים וממתינים עם מצלמה לראיין את קיסוואני לצורכי כתבה. מועד המפגש התרחש יומיים לפני הבחירות לראשות אגודת הסטודנטים והמתח בשיאו, לא רק בין תאי אגודות הסטודנטים השונות אלא גם בין הפלגים הפלסטיניים, שכן מדובר באוניברסיטה יוקרתית בגדה המערבית בה לומדים לא פחות מ-15 אלף סטודנטים מדי שנה בתשע פקולטות שונות. קיסוואני הגיע מלווה בסטודנט נוסף ועלה על המדרכה ובירך לשלום. חלפו שניות אחדות והמסתערבים שלפו אקדחים. קיסוואני התנגד למעצר תוך כדי שהוא זועק לעזרה.

הלוחמים בודדו את המרחב בקריאות מאיימות תוך שהם מנופפים באקדחים, ומנטרלים אותו. בזמן שעוברי האורח והמאבטח המבוגר של האוניברסיטה חשבו שמדובר בקטטה בין סטודנטים, הגיע אל שערי הקמפוס רכב ובו כוח צבאי. ממנו יצאו לוחמי לוחמים לבושים במדים, חבושי קסדה וחמושים ברובי סער שקראו לסקרנים להתרחק. מסתערבי מג"ב לפתו את צווארו של קיסוואני, רצו אל שער הכניסה, עלו לרכב ונעלמו דרך הציר המרכזי של הכפר ביר זית.

יומיים לאחר מכן התקיימו הבחירות לראשות האגודה. תא הסטודנטים של הפתח המכונה "שביבה" זכה במקום הראשון בפער של מושב אחד בלבד על פני ה"כותלה אסלאמיה", תא הסטודנטים של חמאס. מאחור פיגר תא הסטודנטים של החזית העממית המכונה "קוטוב". מעצרו של קיסוואני עורר סערה בגדה המערבית, אך גורמים במערכת הביטחון מיהרו לעדכן כי הוא חשוד בקבלת סכום של 150 אלף אירו ממפקדת חמאס בחו"ל לצורכי פעילות מגוונת ביהודה ושומרון. מאז, חלפה שנה והוא עדיין נתון במעצר.

עד היום, מתנהל ויכוח בקרב הסטודנטים בביר זית. אנשי ה"כותלה אסלאמיה" טוענים שישראל עזרה ל"שביבה" לזכות בראשות האגודה באמצעות מעצרו של קיסוואני, ואילו ב"שביבה" אומרים כי לולא היה נעצר היו זוכים ביותר מושבים באגודה.

חיי לילה ותמיכת חמאס

אוניברסיטת ביר זית היא מוסד פלסטיני להשכלה גבוהה שאת פעילותו החל בערך בשנת 1920 והפך לאוניברסיטה בשנות ה-70, אך יש גורמי ביטחון שיגידו שהוא מיקרו-קוסמוס של החברה הפלסטינית, ויש שמייחסים לתוצאות הבחירות בקרב הסטודנטים לכלי ניבוי פוליטי למה שיתחולל בגדה המערבית בבחירות לשלטון המקומי ולנשיאות הפלסטינית. לכן המאבק בין ה"שביבה" ל"כותלה אסלאמיה" הוא הרבה יותר מניהול אגודת הסטודנטים. מדובר בסוג של מאבק אידאולוגי שאותו מלבים ראשי התנועות השונות, וברוח זו השנאה לישראל הופכת למצע העיקרי בבחירות. ככל שאתה יותר מתנגד לישראל, כך אתה אמור להביא יותר קולות, מה שעלול לגלוש לאווירה אלימה במיוחד.

השאלה היא מדוע אוניברסיטת ביר זית הפכה מוקד משיכה לסטודנטים מרחבי הגדה. הסיבה לכך היא איכותה, המשתדרגת עם השנים והשקעות הבינלאומיות. רק לאחרונה השקיעו היפנים בלימוד מקצועות היי-טק. בטקס הפתיחה, נכח יו"ר הרשות הפלסטינית אבו מאזן. חברות ישראליות התעניינו להשקיע ואף ליצור קשר עם קבוצות סטודנטים וחברות קטנות בראשית דרכן, אך התקבלו בסירוב מוחלט. סיבה נוספת היא הקרבה לרמאללה. אם תשאלו את ראש הכפר כמה תושבים יש בו, הוא יחייך ויגיד: "רשומים? 2,700". אבל במציאות, יש 4,200.

החיים בכפר ביר זית זולים יחסית, וזאת לצד והבילויים ברמאללה הקרובה וחיי הלילה שלה מאפשרים לצעירים ליהנות יותר מהערים, לבלות בפאבים ולשתות אלכוהול. זה מה שלא ניתן לעשות בסביבת אוניברסיטת פוליטכניק שבחברון, שלא לדבר על המכללה האסלאמית בחברון, שבה תעבור שיימינג אם תיתפס כסטודנט כשאתה שותה אלכוהול. שכר הלימוד בביר זית נמצא במגמת עלייה בשנים האחרונות, וכך גם השכירות והשירותים הנלווים בכפר, שהפך למבוקש במיוחד בגלל הקרבה, אלא אם אתה ישן במעונות.

בתוך החלל הכלכלי הזה הגיעו פעילי חמאס. מצד אחד, הרשות הפלסטינית אוסרת על העברת כסף ישיר לסטודנטים של חמאס, אך בפועל מנגנוני הביטחון הפלסטיניים ממצמצים בעיניים כשמדובר במתן מענק לשכירות דירה, מתן אוכל, דמי צילום או רכישת ספרים. כל אלה, בתמורה לחתימה על אמנה של חמאס והתחייבות להיות מעורב בפעילות חברתית. מאוחר יותר, מבינים הסטודנטים שהם נקראים להשתתף בהפגנות, מחאות אלימות ופעילות נוספת שאחריה עוקבים גורמי המודיעין השונים.

רוב הסטודנטים רחוקים מאוד מטרור בפרט ומאלימות בכלל. זו תופעה שהולכת ומתרחבת, בין הסטודנטים ניתן למצוא את ילדיהם של בכירי הפתח. לאחרונה עלתה לכותרות הסטודנטית לנה, בתו של השר הפלסטיני לעניינים אזרחיים חסיין א-שייח. היא הגיעה לקמפוס עם רכב הלנד רובר החדש וחנתה במקום שנוי במחלוקת. לפי עדויות, כשהעירו סטודנטים אחרים היא השיבה להם: "אל בלאד אילנה" - כלומר, זו הארץ שלנו, ועוררה כעס גדול ברשתות החברתיות הפלסטיניות על חוצפתה. השיח המתלהם כלל יצירת האשטאגים "אל בלאד אילנה" ובציניות "אל בלאד לנה". אביה הגיע לאוניברסיטה ומחה בפני ההנהלה על כך שהביכו את בתו.

יורש למהנדס?

למרות הרצון לחיים טובים והשאיפות הקפיטליסטיות לחיי נוחות, והמספרים הקטנים בלבד של סטודנטים המעורבים בטרור לעומת כלל הסטודנטים, האוניברסיטה לא יכולה להתנתק משורת פעילי טרור שיצאו משורותיה. לאורך השנים היו כאלה שחצו את הקווים מהעולם האקדמי לעולם הצללים, בהם גם מנהיגים פלסטינים ובעלי תפקידים בכירים, שהבולטים שבהם הוא בכיר הטרוריסטים יחיא עיאש, אבו אל-ברא, שכונה "המהנדס".

הסטודנט להנדסה הרכיב פצצות מתוחכמות לפיצוץ אוטובוסים ובתי קפה, ולאחר מכן גם חגורות נפץ עבור מחבלים מתאבדים, עד שמצא את מותו בשנת 1996 באמצעות מטען זעיר מתוחכם שהשב"כ פיתח והשתיל במכשיר סלולרי שלו. מהצד השני של המתרס, בולט מרואן ברגותי, בכיר הפתח ומנהיג התנזים שנעצר ונגזרו עליו חמישה מאסרי עולם מצטברים ו-40 שנות מאסר על מעשי טרור שבהם נרצחו ישראלים.

הפעילות והגורמים העוינים בתוך אוניברסיטת ביר זית תמיד נוטרו על ידי קהילת המודיעין הישראלית, אך גם הפלסטינית, שחוששת מפעילות חתרנית נגד הרשות. בשנות ה-80, התקבלה החלטה ישראלית לסגור באמצעות צו צבאי את האוניברסיטה למשך כשנה. הלחץ על ממשלת ישראל והביקורת הבינלאומית סייעו לראשי האוניברסיטה לפתוח אותה מחדש.

למרות זאת, גורמי ביטחון טוענים כי סטודנטים מביר זית מעורבים בהפרות סדר אלימות, בעיקר במקומות שבהם נוכחים כלי תקשורת, גם במעורבות הסתה. מנגד, יש גורמים במערכת הביטחון שטוענים כי לסטודנטים מה"כותלה איסלאמיה" יש גם מעורבות ישירה בהפצת האידאולוגיה של חמאס, שקוראת להשמדת ישראל, וחריגים מהם אף מעורבים בטרור בצורה ישירה.

במערכת הביטחון תמימי דעים כי האוניברסיטה, בראשות פרופ' עא לטיף אבו חג'לה, מהווה קרקע פורייה לאיתור פעילים קיצוניים, שבודדים מהם עתידים להצטרף לזרוע הצבאית של חמאס. לרוב לא יהיה ניתן למצוא אותם בחוד החנית, כמו ברגותי ועיאש, אך הם בהחלט מהווים דמויות מפתח במובנים רבים אחרי סיום לימודיהם לחיזוק הלאומנות הפלסטינית (בערבית: "אנא ווטאני"). חלק גדול מהקיצוניים יעדיפו לתכנן פעילות אלימה ולשלוח אחרים לבצע אותה בפועל.

לדברי גורמים במערכת הביטחון, עד היום לא קם יורש לעיאש, שהוגדר כרב מרצחים, אך באותה נשימה עולה שמו של בכיר ה"כותלה אסלאמיה" אוסאמה אל-פאחורי, אחד ממתכנני הפיגוע שסוכל ביולי 2019 והוגדר על ידי גורמי ביטחון כ"ממשיך דרכו של יחיא עיאש". הוא למד במסלול הנדסה ופיזיקה, וכמו עיאש הוגדר כמנהיג חברתי שבלט ברחבי הקמפוס עד למעצרו על ידי כוחות הביטחון.

מגמה מדאיגה

למרות תשומת הלב, והמסרים שמעבירים מנגנוני הביטחון הפלסטינים ומערכת הביטחון הישראלית לראשי האוניברסיטה, על פעילות שחורגת מהגבול הסביר בקמפוס, רק בשנה האחרונה נעצרו 25 סטודנטים מאוניברסיטת ביר זית. גורם ביטחוני הצביע על סיכול פיגוע בשנת 2017, שבמהלכו התכוונו סטודנטיות לשמש כמחבלות מתאבדות.

ביום ייסוד חמאס השנתי מתקיימת בקמפוס צעידה שכוללת פעילות של רעולי פנים, מדי צבא, וכלי נשק מדומים בהשתתפות של יותר מאלף סטודנטים. במקרים נוספים מתקיימת הצגה על חטיפת חיילים. לדברי גורם ביטחוני, יום ייסוד חמאס מצוין בחסות הקמפוס של ביר זית והוא האירוע הבולט ביותר בכל הגדה המערבית הכולל דגלים, חומר הסתה ותעמולה המוברחים לתוך הקמפוס, ומעת לעת משתמשים בו גם בהפגנות ברחבי הגדה.

האירוע האחרון במעורבות חשוד בפעילות טרור שיצא מהקמפוס בביר זית נכלל בתשתית הטרור שהוציאה לפועל את הפיגוע האחרון במעין עין בובין, שבו נרצחה רנה שנרב. עדיין, את מירב תשומת הלב בשנה האחרונה תופס מעצר בקיץ 2019 של חברי ה"כותלה אסלאמיה", בחשד שגויסו לתשתית טרור ולביצוע פיגועים על ידי הזרוע הצבאית של חמאס ברצועת עזה.

המגויס הבולט ביותר הוא אל-פאחורי, פעיל חמאס בן 22 מאזור חברון ששימש עד לאחרונה כבכיר באגודת הסטודנטים בביר זית. עמו נעצרו בלאב חאמס, פעיל חמאס בן 25 מאזור רמאללה, וכמה פעילים נוספים שהתכוונו לבצע פיגוע מטען חבלה. במסגרת חקירת הפעילים על ידי מערכת הביטחון, התברר כי לפי ההנחיות שהגיעו ממפקד חמאס בעזה היו אמורים הסטודנטים לאסוף מודיעין על מטרות לפיגוע ולייצר חומרי נפץ מחומרים ביתיים. הסטודנטים הצליחו לרכוש חלק מהחומרים הכימיים למימוש הפיגוע.

"זו מגמה מדאיגה", אמר גורם צבאי בכיר בפיקוד המרכז. "מבוצעים באופן שוטף מעצרים של פעילי 'כותלה אסלאמיה' המבצעים פעילות חמאסית גלויה, לעתים מעצרים אלו מבוצעים בתוך קמפוס האוניברסיטה, לאור העובדה כי ההנהלה מאפשרת להם מסתור במקום. כך למשל במרץ 2019, נעצרו בתוך האוניברסיטה תופיק אבו ערקוב וחמזה אבו קרע שעמדו בראש ה'כותלה אסלאמיה' לאחר שקיבלו את אישור ההנהלה ללון במקום. הפעילות הזו ממחישה את מרכזיות ארגון ה'כותלה אסלאמיה' באוניברסיטת ביר זית עבור הנהגת חמאס לטובת מימוש פעילותם הארגונית והצבאית בגדה".

הסטודנט שמעוניין להתקבל ל"כותלה אסלאמיה" וליהנות מזכויות נדרש לחתום על מסמך. "במסמך הוא מקבל על עצמו את האידאולוגיה של חמאס, והוא נכון לפעול במסגרת התנועה, כמעין כותרת כללית לשאר הפעילות שלהם, והוא נכון לקבל סיוע של חמאס בתקופת לימודיו. חשוב להבין שזה הלכה למעשה, גיוס הסטודנט לתנועת חמאס", הסביר הקצין הבכיר.

הוא הוסיף כי "ה'כותלה', שמקבלת כספים רבים באופן יחסי לעומת שאר הארגונים, מצליחה להביא הרבה 'צ'וקולוקים' (הטבות ומתנות לסטודנטים - א"ב), משלב צילומי החומרים, דרך קלמרים, מחברות ותיקים ועד למימון מורים פרטיים. ה'כותלה' הוא כמעט הגוף היחיד שמצליח לארגן את המעטפת החומרית הזו. לסטודנט וככה הם מצליחים לקלוט יותר אנשים ולהחתים אותם".

על החיבור בין תנועת חמאס לבין מה שמתחולל בקמפוס, אמר הקצין הבכיר: "מבחינת חמאס? התנועה מסתכלת על ה'כותלה' כגוף בלתי נפרד ממנה, אחת הידיים של התנועה. התכלית של ה'כותלה' היא קידום רעיון ההתנגדות (בערבית, "המוקאוומה"). ההתנגדות חד משמעית באה לידי ביטוי ב'כותלה' הזו. חמאס מבהירה לסטודנטים שלה שכמו שהם צריכים להיות מצטיינים ב'התנגדות' והם צריכים להצטיין בלימודים. מבחינתם, מי שלומדים הנדסה הם חבר'ה מאוד רציניים, מאוד מתקדמים והם יובילו את עולם התכנון ההנדסי העתידי של חמאס".

חופש ביטוי

לדברי הקצין הבכיר, הנהלת האוניברסיטה מודאגת אך מאפשרת לסטודנטים לפעול באופן חופשי בין כתליה. "מבחינת ההנהלה, היא מובילה מדיניות של חופש ביטוי בגדול והיא רואה את עצמה כאוניברסיטה ליברלית שמאפשרת לסטודנטים לפעול בצורה גלויה. זה מאפשר לסטודנטים ב'כותלה' להוציא לפועל פעילות גלויה ואפילו אלימה", הוא הסביר. "אוניברסיטת ביר זית היא האוניברסיטה היחידה שאפשרה לסטודנטים של ה'כותלה' להופיע בטקס עם מדים צבאיים של חמאס, כולל דגמי נשקים, ולביים הצגה של חטיפות חיילים ישראלים ולהוביל אירועי הסתה ברשתות. בחמש השנים האחרונות ה'כותלה' זכתה במקום הראשון בבחירות למועצת הסטודנטים, מה שמאפשר לחמאס לפעול מתוך לגיטימיות מלאה".

הסטודנטים המצטיינים והאדוקים בדת מגלים מחויבות לחמאס במסגרת פעילויות "רכות" כמו תמיכה חברתית, סיוע לקהילה, עצרות והפגנות, הפצת אידאולוגיה וקידום תעמולה. גורמי מודיעין בישראל טוענים כי הם עוברים לשלב הבא. הם מקבלים משימות צבאיות פשוטות, כמו העברת מידע ופעולות לוגיסטיקה. אם הם יודעים לשלב רמת מידור גבוהה, הם עולים דרגה לכדי פעילות ישירה מול הזרוע הצבאית של חמאס.

יהיו גם כאלו שיתארחו במסגדים וייקלטו על ידי ה"אוסרה" לצורכי למידת תכני דת, אך גם להקמת חוליות טרור, כשהשלב הסופי הוא תכנון פיגועים. במאבק נגד הטרור שותפים מערכת הביטחון הישראלית ומגנוני הביטחון הפלסטיניים, שרואים בהם פוטנציאל לאיום שלטוני.